Robotics Drive Global Production Shift in 2024

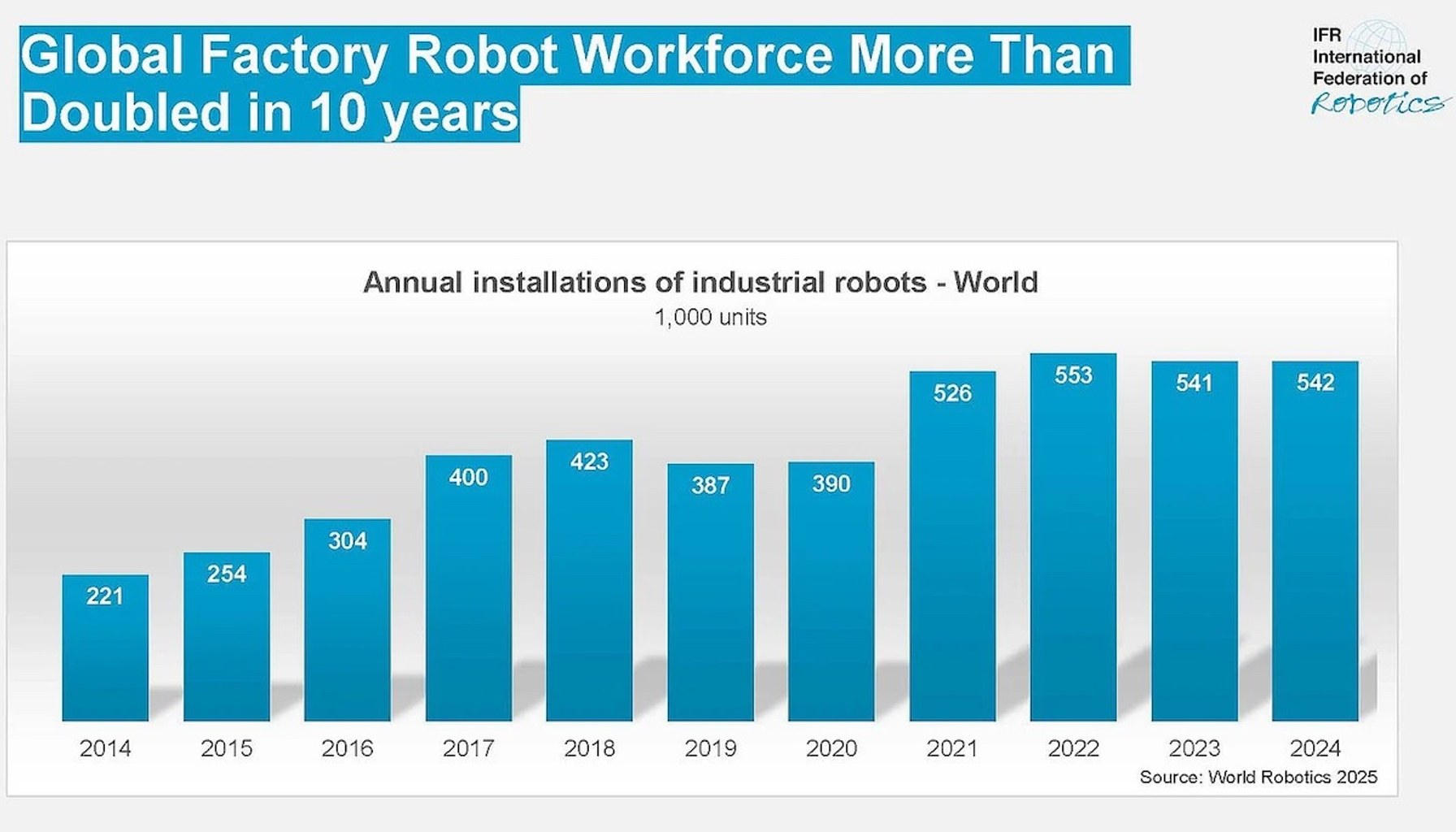

Five countries captured 70 percent of industrial robot sales in 2024. The surge isn’t a tech novelty; it’s a calculated move by manufacturers weighing return on investment, integration hurdles, and the value of speed in production lines. The case study reports 229,000 robotic systems for industrial use were sold last year, a sign that automation is transitioning from pilots to everyday plant floors.

Deployment data shows the concentration isn’t just about budgets, it’s about policy and market structure. Japan, China, the United States, Germany, and the Republic of Korea are driving the bulk of demand, underpinned by a mix of national programs and private capital flows. The United States, notably, relies more on private capital than federal funding, signaling a demand-driven push from manufacturers who see automation as a lever to either outrun rising labor costs or shrink cycle times enough to reclaim margin. The breadth of the sector is large: more than 343 companies manufacture industrial robots, and around 347 systems integrators help tie those machines into actual production lines. The market for service robots is expanding too, with professional-use robots totaling 24,207 units last year, and military and other special-purpose deployments accounting for a sizable portion of that professional service segment.

The numbers aren’t a victory lap; they are a reminder that automation is a business decision, not a miracle cure. Plant managers are increasingly measured by cycle times and throughput, two operational metrics that signal real ROI beyond shiny demos. In practice, this means automation projects are evaluated through the lens of how fast products move from input to finished goods and how many units can be produced per hour without sacrificing quality. The data imply that firms investing in robotics are prioritizing predictability and uptime as much as speed. In other words, the speed of a single line is often the gateway metric to a broader productivity story.

Automation remains a central hurdle beyond the hardware. Automation deployments must splice cleanly into existing production ecosystems (think ERP and MES connectivity, data sharing across equipment, and reliable cross-platform signaling). In many plants, the value of a robotic cell collapses if it cannot talk to the rest of the factory stack, generating blind spots and underutilized assets. The case also underscored the reality that these projects are capital-intensive and require careful planning around maintenance, software updates, and cybersecurity. Without a well-mapped integration plan, the upside from faster cycle times and higher throughput can erode as soon as a line goes offline for a software patch or a control-system mismatch.

The role of skilled labor in automation, while not the headline here, is a real practical constraint. Automation programs tend to augment craft labor, maintenance staff, quality inspectors, and line engineers, rather than entirely supplant them. Successful deployments typically hinge on training and change management, ensuring technicians understand how to troubleshoot, calibrate, and tune robotic cells while operation remains stable. Without this, even the best robots can sit idle, awaiting a skilled technician or a software fix.

Looking ahead, plant managers and CFOs should watch three threads. First, capital availability will continue to shape how aggressively plants scale automation from a pilot in a single line to an enterprise-wide program. Second, policy and supplier ecosystems in the leading countries will influence the pace and cost of deployment, especially as integrators mature their capabilities. Finally, the interoperability of new robotics layers with existing data systems will determine whether ROI comes in as expected or requires a mid-course correction. The trajectory is clear: automation is reshaping production, but the most consequential gains come from disciplined execution, integrated systems, measurable cycle times, and a workforce prepared to run, fix, and optimize the new normal.

- Modernizing the global economy with industrial robotics is needed but not inevitableThe Robot Report / Independent source / Published JUN 14, 2026 / Accessed JUN 15, 2026